Refinance twice with the same Bank under MAS many many guidelines.Originally Posted by Amber Woods

Senior

Senior

Refinance twice with the same Bank under MAS many many guidelines.

Senior

Total debt is 428K+660K+750K.

PC bought without CPF money.

HDB use CPF for 200k 25 years loan.

Property on hand.

5 room 126 sqm HDB at Balam road 370027

Southbank 2 Bedroom 958 sqft 198784

Terrasse 1453 sqft 3 Bedroom PH. 544780

Last edited by Arcachon; 26-07-17 at 10:47.

Amber

Amber

In 2011, you met all the MAS's requirements and that was when property prices were at 2011 high. You should be fine as long as you pay your monthly mortgage faithfully. If you miss any payment especially if property prices decline further and causing hardship, you will find yourself having to sell at least one of your property.

So your total debt is $1.8m. Keep finger cross property prices will not crash on you and you can continue to pay your mortgage faithfully.

Ultimate Underdog

I don't think it is difficult to sell a Terrasse penthouse for 1.3m at today's market. It is probably valued at 1.5m today or more.

Market index down 30% doesn't mean all property down by 30%.

I see the market as not-up (=down) for the last 4 years, presenting itself as "already down by more than 30%". Many compromises in final product offering were made to "create" this down effect. Overpriced CCR were forced to correct massively, developers were squeezed to offer cheaper products (and poorer finishing) to manage costs, "unusable" areas by proportion has continued to go up as sizes of properties shrink, and older properties sellers (who have bought at yesterday's prices) were forced to accept disproportionately lower prices, just to name a few compromises in the equation.

Any lower will cause supply to shut off almost completely (even from the older properties group). I believe cost-push factors will continue to inch the prices upwards from this point.

The three laws of Kelonguni:

Where there is kelong, there is guni.

No kelong no guni.

More kelong = more guni.

Senior

You are right, that is why need to keep repeating to myself what I having. Thank everyone for bearing with me all this years.

Ordinary Account (OA) $128,289.61

Special Account (SA) $113,035.74

Medisave Account (MA) $49,796.17

$1,020.00. (*OA: $413.62 *SA: $317.01 *MA: $289.37)

$189,820.72 Net Amount Used

$ 70,680.29 Accrued Interest

$260,501.01 Total

Date Of Application 25 Oct 1993

Date Of Purchase 01 Nov 1995

Purchase Price $225,600

Loan Commencement Date Nov 1995

Loan Expiry Date Oct 2020

Interest Rate (p.a.) * 2.60% (Concessionary)

Monthly Instalment $923.00

I pay $600

Wife pays $263

If you pay off your mortgage of $41,168.80, your interest savings will be $2,174.80.

3 years 11 months

Newbie

Southbank was bought for below 600k (600psf) and today is 1.5m (1500psf)

-------------------------------------------------

30 Jun 2006 881#25 - xx904 sqft84 sqmS$548,000(S$606.08 psf)

30 Jun 2006881#27 - xx958 sqft89 sqmS$585,000(S$610.66 psf)

30 Jun 2006881#27 - xx904 sqft84 sqmS$561,000(S$620.46 psf)

30 Jun 2006881#28 - xx958 sqft89 sqmS$607,000(S$633.62 psf)

30 Jun 2006881#28 - xx614 sqft57 sqmS$463,000(S$754.63 psf)

30 Jun 2006881#28 - xx1,313 sqft122 sqmS$808,000(S$615.29 psf)

and today transacting around 1.5m (slightly less)

17 May 2017881#18 - xx592 sqft55 sqmS$878,000(S$1,483.07 psf)

24 Apr 2017881#25 - xx958 sqft89 sqmS$1.450M(S$1,513.59 psf)

14 Dec 2016881#34 - xx958 sqft89 sqmS$1.450M(S$1,513.59 psf)

9 Nov 2016881#16 - xx969 sqft90 sqmS$1.446M(S$1,492.64 psf)

Newbie

other 2 properties on rental?

Senior

Southbank 4K

5 room HDB 2.8K

Staying at Terrasse, not many ten years left.

428K 67th Instalment 04/01/2016 $1,551.84 1.68% $349,803.32

660K 56th Instalment 04/01/2016 $2,386.19 1.68% $555,732.84

750K 18th Instalment 04/01/2016 $2,928.03 1.68% $732,172.35

Last edited by Arcachon; 26-07-17 at 11:07.

Newbie

the high rentals of 2010-2013 was an anomaly. rentals today are normalized values, they didn't crash. for CCR condos or even RCR, getting tenants not difficult.

but of course, let's put it in perspective.

if you have 100m worth of funds, then yes, you're right to go for 50:50 asset allocation. You're considered HNWI already. probably have a sentosa cove property.

but for normal individuals who need to leverage up, who needs time to build up assets passively, singapore property is a fine way of doing it.

my personal opinion of course.

Newbie

thanks for so openly sharing. salute.

Global recession is coming....

As you rightly mentioned, that is US lah, stupid!

In US you can accuse the Presidents like Trump for committing cronyism and nepotism because he appointed his family members and his cronies to key positions and trying to enrich himself and trying to hid his income tax filing and nothing will happen to you!

Well, you can try that in Singapore and see how????

Senior

May be I was lucky with 4 tries at the low. I believe property is an art as well as science. Plus luck.

Newbie

Bro, can u pass us your 4D no and your luck?

Need luck and actually for most people, circumstances that land up at the right place at the right time

Newbie

That is more than max leveraged.

Newbie

I have consistently been saying, buy property but know the risks. And buy prudently!

I am only responding to Laguna's post.

Every individual's property portfolio is different. The properties are acquired in different times, with different entry prices. So it is normal to assess the portfolio weight from time to time.

The goal of an investor is to maximize return of money deployed. There are so many investment options, property is but one. For example, I mentioned AUDUSD coincidentally the other day; it is amongst the currency pairs that I trade regularly. It turned in a monster return just recently.

Senior

Last property purchase was in 2010. Shifted to equity in three major markets by leveraging on the law of averaging. Saw 70-80% gain and took profit recently as one should not be too greedy but the bull is still charging. Waiting for opportunity now but into property.

Senior

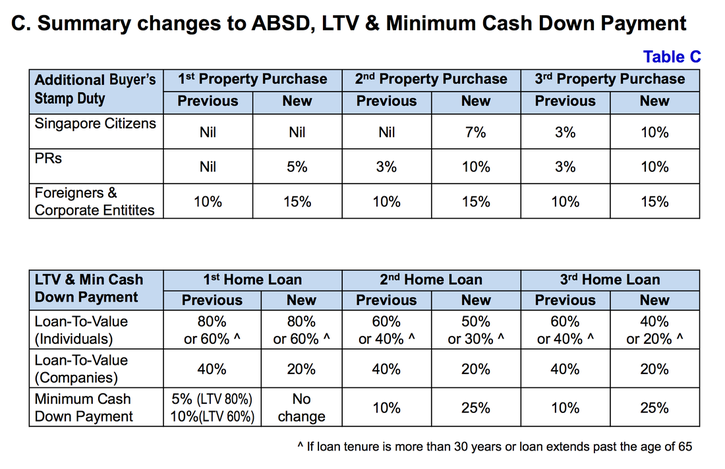

10%+(3%-5400)

http://www.100qns.com/absd-guide.html

Senior

It is sure lose for multiple properties owner and giving money to garment. It is better to invest this money in other vehicles at least still have some returns.

Newbie

Since these financials are shared publicly, can I borrow them to illustrate?

The structure of a typical property investment is really straight forward.

You put up a sum of money and borrow the rest to fund a purchase. The total sum becomes the working capital. The key is the working in working capital.

The sum of money put up is the equity to cushion a potential fall in the property value after having purchased it. How much to put up is a calibration of potential risk assessed in a property cycle, and therefore a measurement of the amount of leverage.

For example, 20% money put up with 80% bank borrowing means a leverage ratio of 4.

(

Therefore, the structure of a property investment is the same as trading. Leverage is involved, it is just the degree of leverage.

The difference is the leverage ratio of the underlying instrument; for example a trade of currency the leverage ratio is 40, for stock index the leverage ratio is 20.

The difference is also in the time duration of the trade.

Property investment is simply a trade of 20-, 25-years etc. It is just an open trade until it is closed, until the property is sold. It is called an investment just to make it sound more atas.

)

The rental income, the cash inflow is to be used to fund the mortgage payment. At the end of the loan tenure, the property is fully paid for.

Simple.

Now how about applying this simple process here?

If we add up all 3 properties to consider them as one property, then the total sum borrowed is $1.8 mil.

But $1.3 mil out of $1.8 mil is actually money that is non-working, because Terrasse is for own-stay purpose.

Secondly, out of the amount of equity put up, almost $500 k (being Southbanks real equity) is not locked in. This, as Amber highlighted, is exposed to market condition.

Senior

I am happy to let you share but remember to link to this forum the reason being not many will believe what you share.

I was in United State when 11 Sept 2001 event happen and witness the history changing event on site, the next day one News article wrote that after a few years people will start to believe the event was not truth and it was some Hollywood movie.

Being a Christian I believe the News and I start to read about the New Sept 11. Christ die for the sinner and those who believe in him is willing to give their life but after so many years how many believe it is truth.

Spend 20 week in the land of Milk and Honey and to see first hand where Christ leads to Crucifixion, there are still so many un believers.

Last edited by Arcachon; 30-07-17 at 20:15.

Senior

You need to watch this to understand what and how I think.

Nothing complicated, simple believe money printing is beyond control.

All the bull shit is just to hid the money printing from the World.

Tell me what you know about "Who controls the money supply and who print the money."

Newbie

If I pay 500k less to stay in PP compared to QT, and yet I am in city fringe, why not.... U know how many years we need to work to save 500k? Owing this money means we reduce on lifestyle for years, and I don't tink tis is a good way of living....provided u have 500k to spare without feeling a pinch!!! And for QT, the price is easier to go down than go up . And the reason for such a difference have to do with QT is a more matured estate and nearer to town. And developers spoil the market by bidding too much, and people are suck in by fear..... u see those who bought ascential sky, didn't resale at 2k psf, but resale at your purchase price, means ....next time u resell your Commonwealth towers, Queens Peak will either at your purchase price or lower, good luck to those who bought!

Last edited by henryhk; 30-07-17 at 23:46.

Newbie

Perhaps they see the home as a utility rather than an investment. While they purchase QT for $500k, when it comes time to sell they will also be able to sell it for +/- $500k more than PP. Anyway i think with today's high prices for housing and so much uncertainty in jobs, it is difficult (although not impossible and not the choice of many) to stay in the job for 30+ years just to pay off the housing loan.

Junior

Not all RCRs are equal. Just like not all CCRs are equal and not all OCRs are equal.

Amber

I am not an economist but do understand some basic economics which I hope Leeds or some other experts can correct me if I go out of line.

As a consumer, we should not be looking at the supply side (central banks) of money and try to base our decision making in buying property. As individual, we cannot influence the economy but instead we suffer from the changes in the economy. Central bank uses monetary policy and government uses fiscal policy and collectively they try to manage the economy.

As an individual, we should be concern with income and debt. Our income generated from our assets and earnings from being employed must be able to finance our debts.

Unlike in the US where one could walk out of the housing loan without further liability even if the mortgage is greater than the value of the house. In Singapore, your housing debt remains even after the forced sale of your home if the sale proceed cannot cover the mortgage. Hence, the approach to housing loan must be prudent because housing prices can boom or burst during the economic life span.

To be prudent, we need to manage our cash flows in any investment, especially so in property which is illiquid. If we cannot afford negative cash flow for an extended period of time, then we should review and take action now. We must not live and hope that the property prices will continue to rise or maintain its value. This is the assumption that most people make when buying property and get themselves into trouble.

Most savvy investors will not get into trouble because they know when to enter and get out of the market because they know the amount of risk they can take. They do not necessary buy at the lowest price or sell at the highest price. Greed kill!

Of course, there are also many rich individuals who buy properties to keep and they never need to worry about the up and down. Having said that, most rich people actually don't do that or how then they become rich in the first place.

Newbie

The assumption is that QT is more valuable than PP & the same premium would continue into the future.

And not all have intention to pay the loan fully, meaning if the underlying value exceed the purchase price, will cash out & move on.

Junior

Property and cash is similar to tortoise and hare race. Tortoise (property) is slow but consistent, while hare (cash) is fast but lazy. In the beginning hare maybe fast at the starting lines, but consistent tortoise win at the end. Life is never a sprint, its a marathon.

Global recession is coming....

Well well, isn't that what I said all along?!

Just buy a freehold property in CCR correct location and then sleep on it and you will do much better than anybody else who don't 50 years down the road (in the long run)!

This way of investing will significantly beats those who tries to flip their 99-years leasehold property every 10 years (or less)! - These people only benefits the Gov coffers with ABSD, SSD, extra stamp duties in replacement purchase and also the agents collecting fat agent fees.............

Senior

A FH Unit at Astrid Meadows bought in 2005 sold for $3.1 million profit (extracted from the edge property dated 31 July 2017.

Newbie

Nice place, astrid meadows. they don't make them like they used to anymore.

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote