別說沒警告你!七大佬看空美股:逃!

https://www.facebook.com/57ebc/video...rczhXb_gGo5C2Y

Senior

Senior

別說沒警告你!七大佬看空美股:逃!

https://www.facebook.com/57ebc/video...rczhXb_gGo5C2Y

Newbie

Newbie

If need to sell shares to buy property, I tink better don't buy.... must have deep pockets then can buy

Senior

True, now with ABSD most go into share. Better get out fast.Originally Posted by henryhk

Newbie

No, Singaporeans usually shun shares, many still buy pricy properties and pay 10% ABSD....

Global recession is coming....

Most people I know (and also those I heard from relatives and friends) are doing what you said: shun shares and buy pricy properties (even if need to pay 10% ABSD)!

Is it any wonder why OCR private property prices are at THOUSAND years historical PEAK price?

Senior

same here. hardly know anybody who invest in shares, let alone invest a lot in shares (an amount that is enough to pay just 20% of a property). they either bought properties, bonds or kept the money in cash. I know of quite a few who have an investment portfolio of > $1m but would allocate < $200k to stocks.

Newbie

At tis time, property overpriced, gone are the days where u can make 300k profits by holding and flipping, ...it is wiser to buy good shares and earn dividend , while waiting for price to go up, tose who bought Last year know wat I mean.... and selling is just a press of a button, don't need to wait for buyers! Instant!!! My point is don't put all the money in one basket and pay high interest rate !! Anybody pay 6.75 percent befo.....I have

Newbie

Same view. That's why we want to offload out 1st property and buy a 2nd one. This one is bought at a high. Yet, I still see people buying properties as investment now.

We are prepared to sell at cost rather than to rent. Since rental yield isn't looking good too.

Newbie

shares can tank and tank fast. i did well in 2000-2007 for shares, after that was iffy. some of my REITs were badly hit two years ago. i really think singapore property is safer than stocks, there is always a tenant pool no matter what. as i get older i rather not risk too much in stocks.

Senior

Because OCR Thousand years ago got Tiger and Lion running around eating human.

Newbie

I have a different experience, bought a lot of shares after financial crisis in 2007 because it was so cheap and don't want to miss the boat and make a sum of money. Use it to buy and flip 3 properties from 2009 to 2013, because property runs faster than stocks... Property also tank v fast too and silently, tats why befo 2007 i was out of property, as I am holding one illiquid asset, for stocks u can set cut loss target, and the amount is less than 1/3 of property, so is not as scary as u thought.

Senior

I think Max 3.5%, otherwise MAS is sleeping.

6.75% are history, where the World was told cannot print money but after 2008 GFC everyone join the party.

"selling is just a press of a button, don't need to wait for buyers! Instant!!!"

I must be living in the well for too long, did not know now share can sell by just a press of a button, don't need to wait for buyers! Instant!!.

Last edited by Arcachon; 13-08-17 at 15:39.

Newbie

nah, i don't think shares are as safe. you can look at keppel corp, the speed in which in tank in december two years ago can make any investor sheet bricks.

the problem with property is if you got margin call . if one are not over leverage i prefer hard property (singapore).

the worst is the counter you holding kanna CAD probe, trading halt, you lan lan money stuck there. after 1 year trading resume at 10% the price. lost almost 10k just like that, money thrown down drain.

so for me stocks only 5-10% of my net asset, not more than that.

Newbie

Agree, I don't mean to say stocks 50% of net asset, buy at your comfort, ......the % u decide, but is an alternative investment to properties..... thanks for reminding me kepcorp, I cut loss 2k wen it goes against me and move on, makes more on banks and other blue chip stocks.... not tose CAD penny stocks,

Ultimate Underdog

I find it hard to control emotions linked to decisions about stocks when the amount per stock goes beyond 30k and the total portfolio exceeds 100k. So the moment it hits over 150k or 200k it will go into real estate.

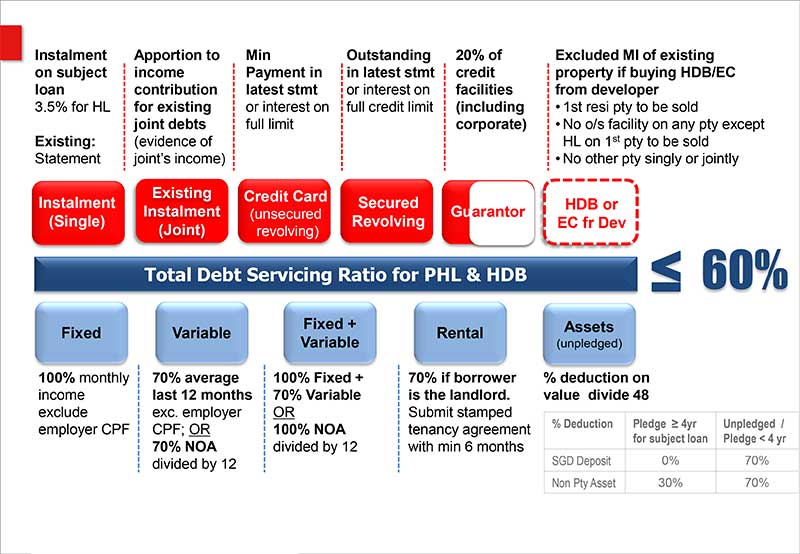

It's getting harder with the TDSR, LTV and ABSD.

The three laws of Kelonguni:

Where there is kelong, there is guni.

No kelong no guni.

More kelong = more guni.

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote