How old are you.Originally Posted by Werther

Any bank that give you the best rate.

Have been with UOB since 2006, 1.38% about 1.5 million loan.

Senior

Senior

How old are you.

Any bank that give you the best rate.

Have been with UOB since 2006, 1.38% about 1.5 million loan.

Newbie

Bro, i m in early fifties.

UOB rate so low?? 1.38%.

OCBC i m now paying 2.11%

Senior

Time to look for another bank.

Senior

Cooperation is the in word now, gone were the day agent kill one another.

If you got bad experience with agent before do come and experience how Agent can help you.

No use keep crying all agent the same, one don't have a lot of 10 years to cry.

Many of my external cobrokes and buddies outside of Propnex had heard about the Dynamic Wealth Creation Program that I have put together. We are suppose to have coffee/tea to exchange ideas. However, everyone are always on the move, much less sit done for a few solid hours.

This coming Friday, organized by POC Dynamic Force Group, I will be sharing with my POC Group Agents some of the key techniques.

I have decide to open to all my Non-PropNex and my teammates Non-Propnexian friends too. (Good or not? ��)

Due to seating capacity, do let me know in advance if you will like to join me. Lets catch up before of after the sharing. Cheers!

For Propnexians who had heard many positive feedback about this sharing that I had shared with several groups already, do be patient. I hereby promise to do another round for you guys during one of the Winning Wednesday.

Happy closing to all my FB Agents friends.

Senior

Senior

Senior

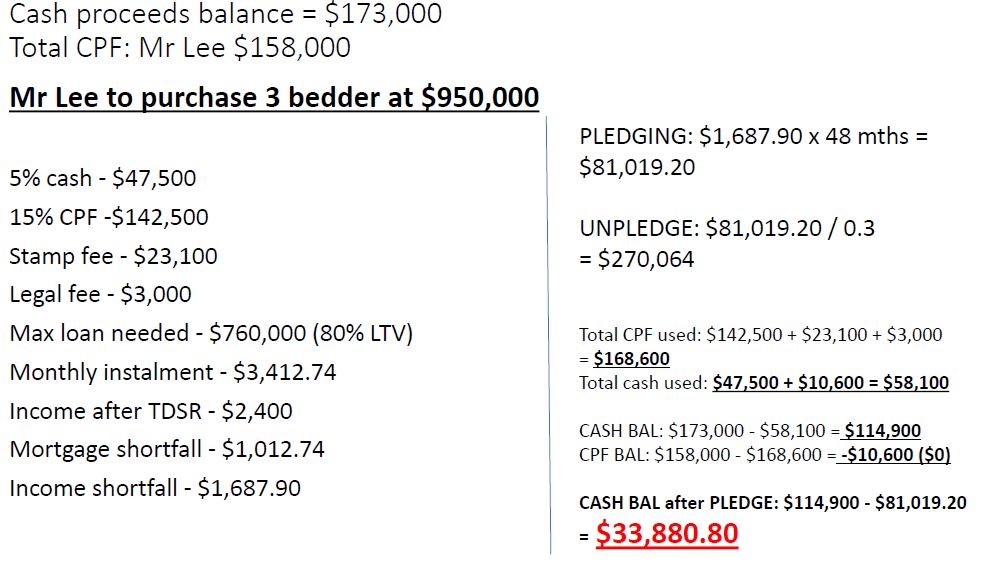

TDSR income = 4000 x 0.6 = 2,400

Loan required 668,000

Monthly 3,000

shortfall = 3,000 - 2,400 = 600

income required for TDSR = 600/0.6 = 1,000

need to put FD = 1,000 x 48 = 48,000.

Senior

Senior

Senior

Senior

Senior

Senior

Senior

De-coupling and Part-purchase

One method for a couple to avoid paying ABSD on a second residential property purchase is to do what is known as a de-coupling and part-purchase of the ownership of the first property. This essentially involves removing one spouse from the ownership of the first property. That way, he or she can buy a new property without paying ABSD for what is a second property owned by the couple. What does this entail?

As most married couples purchase their matrimonial home as joint tenants, de-coupling results in Spouse A becoming the sole owner of the existing property and Spouse B purchasing a new property. This would require the following steps:

1. Severance of joint tenancy

This requires the signing of an instrument declaring the severance of joint tenancy in the property. Your lawyer will prepare this instrument in the required forms for your signing, and subsequently register it with the Singapore Land Authority.

2. Part-purchase of one spouse’s share in the property by the remaining spouse

This means that Spouse A buys over all the shares owned by Spouse B in the property. This is commonly known as part-purchase because Spouse A is purchasing only a part of the property, since he/she already owns the other part. A part-purchase typically requires the following steps:

Transfer of ownership through a Sale and Purchase: This works exactly the same way as a normal sale and purchase. A sale and purchase agreement will have to be signed by the parties, and the agreement will have to be stamped.

While a transfer of ownership can also be effected by way of a gift by Spouse B to Spouse A of his/her share, it is advisable to go through with a sale and purchase instead. This is because a transfer by way of gift may be set aside as a transaction at an undervalue in the event of bankruptcy. This may have negative implications for the owner looking to sell the property, as it may be more difficult for the potential buyer to obtain a bank loan.

Stamp duties: Stamp duties have to be paid within 14 days of the execution of the sale and purchase agreement. BSD will have to be paid, based on the purchase price (or the market value, whichever is higher) of the share of the property being transferred. If the property was purchased less than 4 years ago, then Spouse B will also have to pay Seller’s Stamp Duty (SSD). Again, what is payable is also on the portion of the property being sold (ie, if Spouse A is buying over 1% of the property from Spouse B, then what is payable is on the purchase price/market value of that 1%).

Refund of CPF monies: All CPF monies used by Spouse B towards the purchase of the property will have to be refunded to his/her CPF account together with accrued interest upon completion of the sale. Your lawyer will also have to help you apply for a partial discharge of the CPF Board’s charge over your house, such that Spouse B’s name is removed. The refund of CPF monies can usually be completed within 10 working days of the sale, freeing up Spouse B’s CPF funds for the purchase of a new property.

Restructuring and refinancing of bank loan: If you financed the purchase of your property with a bank loan, you will need to speak to your banker about restructuring or refinancing of your home loan. This will typically involve removing Spouse B’s name from the loan. If you are looking to refinance with a different bank, you may find more tips and pointers here. If you are looking to complete your part-purchase within a shorter period of time, it may be easier to refinance with your existing bank, as they are more likely to allow for a shorter notice period for redemption of your existing loan if your new loan is also with them.

Similar to a normal refinancing process, your lawyers will also assist you in discharging the existing mortgage for the old loan and lodging the mortgage for your new loan.

Upon completion of the above transactions, Spouse B can go on to purchase another property without paying ABSD. This is because he or she no longer owns any property.

However, de-coupling the ownership of Housing Development Board flats might not be possible because the Housing Development Board (HDB) revised their regulations on 1 April 2016 to restrict the transfer of flat ownership. Flat owners will be allowed to transfer the ownership of their flats under six circumstances including marriage, divorce, death of an owner, financial hardship, renunciation of citizenship and medical reasons. All other reasons will be assessed by HDB on a case by case basis. More information on the new HDB regulation can be found here.

https://singaporelegaladvice.com/law...rs-stamp-duty/

Senior

Senior

wah, they copy your slogan.

Senior

Not me, from facebook.

Senior

Mother 70, Daughter 40.

Cash on Hand 700k.

self stay property o/s loan 700k.

How to buy another property without ABSD.

Ultimate Underdog

Transfer to Mother with loan capped at 50% valuation. Possible?

Use remaining funds and 40 YO profile to loan and buy.

The three laws of Kelonguni:

Where there is kelong, there is guni.

No kelong no guni.

More kelong = more guni.

Senior

https://propertynet.sg/cashing-out-p...e-equity-loan/

https://www.mortgagewise.sg/tdsr-removed/

What is equity term loan (ETL)? This is strictly not at purchase, but refers to the additional loan that is taken out against the property valuation on the part which has been fully paid for over the years. And there is a condition – the equity loan portion does not comprise more than 50% of the loan-to-value (LTV).

Senior

even then the monthly cash repayment for the mother for the 700k loan also face green green already.

Ultimate Underdog

Servicing one loan of 700K with no tenant versus 2 loans of 350K plus 350K and having a tenant help to pay for 1 to 1.5 of the loan. Which is better?

The three laws of Kelonguni:

Where there is kelong, there is guni.

No kelong no guni.

More kelong = more guni.

Senior

OPM or no OPM there is a different, not many understand.

Our government know and understand that is why they need to stop people from OPM otherwise no worker everyone OPM.

Senior

Husband 38 years old, wife 35 years old own condo bought 2011 $1,200,000.

Husband SC wife SPR.

80k cash, 200k in CPF 50/50.

30 years loan outstanding loan 800K

Husband income $8,000 Wife $7,000

Husband OA 50K wife OA 100K

CPF refund with accrued interest is 150K husband 180K wife

50K cash FD and 100K in stock

Current valued at 1.8 million.

Senior

Senior

Singapore, 10 March 2017

http://www.mas.gov.sg/News-and-Publi...-Property.aspx

We will no longer apply the TDSR framework to mortgage equity withdrawal loans with LTV ratios of 50% and below.

Singapore, 5 July 2018 ---- Raising Additional Buyer's Stamp Duty Rates and Tightening Loan-to-Value Limits to Promote a Stable and Sustainable Property Market

http://www.mas.gov.sg/News-and-Publi...ue-Limits.aspx

with effect from 6 July 2018 ---- GUIDELINES ON THE APPLICATION OF TOTAL DEBT SERVICING RATIO FOR PROPERTY LOANS UNDER MAS NOTICES 645, 1115, 831 AND 128

http://www.mas.gov.sg/~/media/MAS/Re...nes_050718.pdf

Senior

99% 1%

When to use this?

Senior

https://www.mortgagewise.sg/decoupling/

Condo Valuation = $1.5m

Selling Price = 50% = $750,000

Existing Housing Loan = $700,000

Mr Tans CPF used todate (plus accrued interest) = $150,000

Mrs Tans CPF used todate (plus accrued interest) = $10,000

Mrs Tans CPF Ordinary Account Balance = $250,000

Financials For Seller (Mr Tan)

To sell 50% stake and receive $750,000 as follows:

Loan to be redeemed = $350,000 (also 50%)

Goes back to his CPF = $150,000

Cash proceeds = $250,000

Financials For Buyer (Mrs Tan)

To refinance her own 50% loan of $350,000 to the new bank

(at same time) Buy over 50% stake and pay $750,000 with breakdowns below.

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote