PROPERTY NEWS2 hours ago · 8 min read · by Ryan Ong

HDB resale market: 4 key predictions for 2019The idea of a HDB resale flat has taken on a lot of emotional baggage lately; blame it on public and media conversations about 99-year leases. And while thereve been

a healthy volume of resale flat sale transactions in the last quarter, transaction prices in the HDB resale market have remained stagnant. But at the same time, private property are on the pricey side right now, with many condos out of reach for many first-time homeowners and even upgraders.

With many sellers and buyers stuck between a rock and a hard place, wheres the HDB resale market to go from here? Well, heres what you might see come 2019:

The situation to dateAs we mentioned, the volume of resale flat transactions has gone up. According to URA numbers, there were 7,063 units sold in third quarter of this year. Thats an increase of about 21% year-on-year, creating one of the highest peaks in HDB resale transaction volume since 2010.

Regardless, resale flat prices are mostly flat. Overall resale prices slipped 0.1%, undoing a 0.1% gain in the second quarter.

Moving forward in 2019, were likely to see more of the same, unless Brexit and Sino-US trade tensions end up wrecking the market. Were on the verge of seeing the outcomes of these events.

Here are 4 things were likely to see for HDB resale market in 2019:

- Tighter LTVs for private bank loans could bolster the HDB resale market

HDB resale flats have started to look more affordable, at least relatively, thanks to the last round of cooling measures.

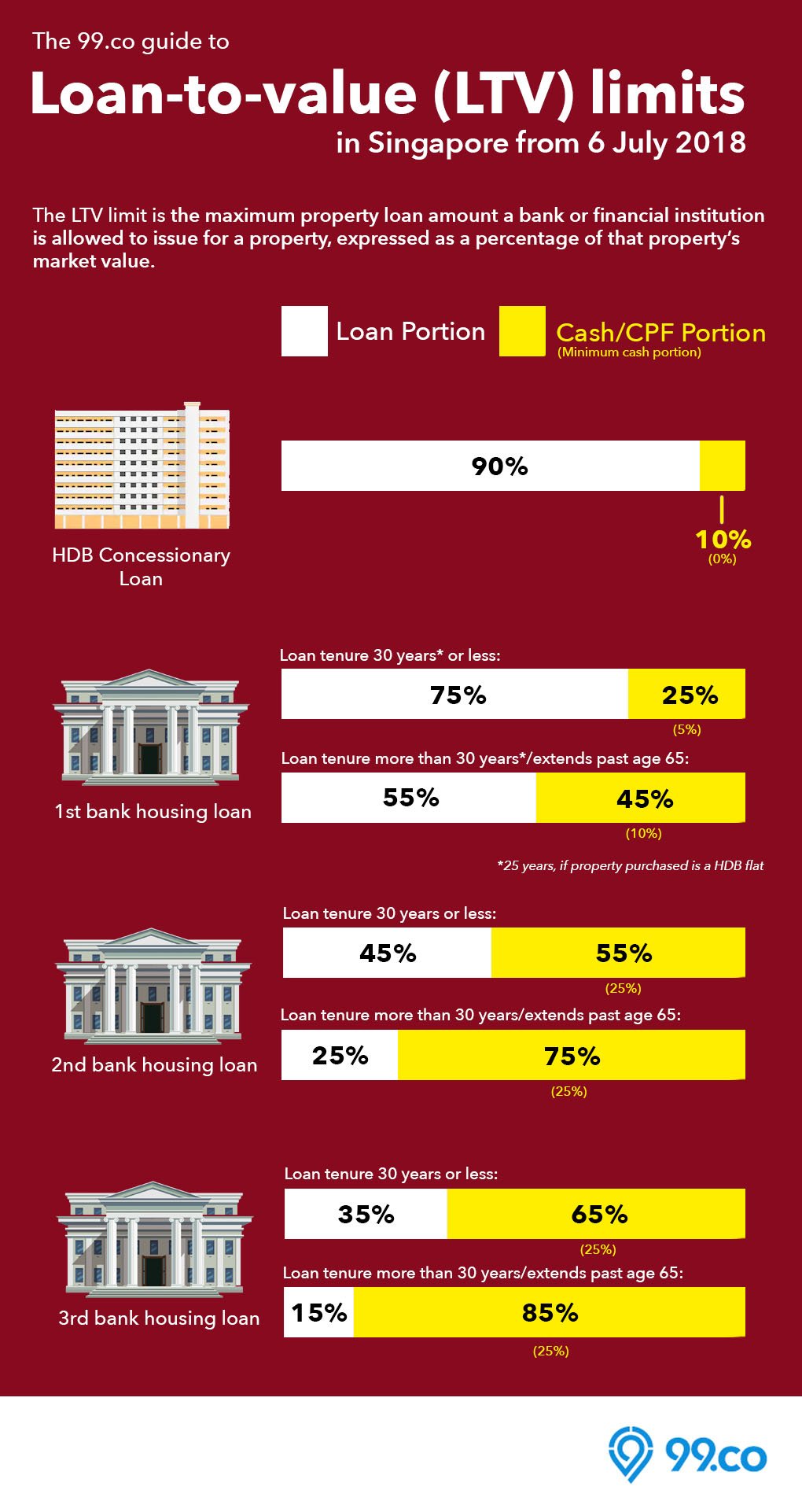

Even first-time buyers of private property now have a maximum Loan to Value (LTV) ratio of 75%, down from 80% before the cooling measures. For a mass market condo in the $1 million range, this is roughly another $50,000 needed in cash or CPF. (5% of the downpayment must be in cash.)

That said, buyers of HDB resale flats can still turn to

HDB Concessionary Loans, subject to eligibility conditions. HDB loans can finance up to 90% of the flat price, with the remaining 10% coming from cash or CPF (with no minimum cash amount).

This makes a huge difference for new couples, who typically have a lot of costs to plan for (e.g. first child, first car, wedding debts). The lower cash outlay from an HDB loan may be justification enough for them to seek out a HDB resale flat for a first home instead of a condo, especially if they exceed the income ceiling to qualify for a Build-to-Order (BTO) flat, or are tired of balloting unsuccessfully for one.

In fact, the group of sandwiched Singaporeans who bust the income ceiling for a new flat, but are not wealthy enough to manage private property prices, is in significant numbers. They are simply unable to stomach the added 5% downpayment to buy a condo.

We expect the lower cash outlay needed for resale flats will continue to be attractive to first time buyers, sandwiched buyers, and some upgraders, and this will keep demand for HDB resale flats from falling below sustainable levels. This could just be enough to prevent further downward price pressures for the HDB resale market.

LTV ratios favour HDB buyers.

- But, at the same time, we wont see the same enthusiasm for older resale units that we saw back in 2013

While many of us assume that older flats in mature areas have always been valued higher, this isnt true.

The trend of paying more for older flats really began in 2002; that was when public awareness of the benefits of certain HDB schemes, such as the Selective En-Bloc Redevelopment Scheme (SERS, originally announced as far back as 1995) really started to kick in.

From there on it started to climb, and by the time of the last property peak in 2013, Cash Over Valuation (COV) in the amount of $30,000+ wouldnt have raised a single eyebrow.

Were raising this reminder for two reasons:

First, remember its not an inherent or fundamental fact that older flats are always worth more. Sentiment is a big part of it, and that can change. Our valuing and sometimes overvaluing of old flats is something that began less than two decades ago, and one of the main causes was SERS.

We dont dispute that key attractions of older flats are size and amenities but there also used to be the lingering belief that, if the lease ran out, SERS would kick in and rescue the situation.

With the announcement of

VERS, and the fact that only around 5% of estates today qualify for SERS, that belief that is now quashed. Instead its replaced by fears of

what will happen when the 99-year lease runs out; along with debates about whether you truly own your HDB flat.

We dont have many details on VERS yet, but we know for a fact that it wont be as generous as SERS, and that it will be voluntary, which means it may not even go through if your neighbours vote against it.

All in, theres now much greater awareness, of what could happen when your flat gets too old. The shorter remaining leases on resale flats will now weigh more on buyers thinking, and it could put a dent in the demand for older units and even force prices down.

That said, ageing flats in close proximity to key amenities, such as MRT stations and good schools, may still see a healthy demand as the owners can realistically utilise the units for a decent average rental income after the five-year Minimum Occupation Period (MOP) given they can afford a second property.

Ageing HDB flats close to the MRT station may still see a good demand.

- Theres only one EC launch in 2019, which could help sustain HDB resale demand due to lack of options

Coming back to sandwich-class Singaporeans, many of them tend to choose between Executive Condominiums (ECs), and big resale units.

For 2019, theres only one EC launch, at the Sumang Walk area in Punggol. We wont rehash the quibbles and controversy over this development, except to point out a number of people feel its expensive. Were talking a million dollars for a three-bedroom unit, in

Punggol.

Thats not to say its bad of course, its waterfront living (next to the Punggol Waterway). The Punggol Digital District could also raise value of properties in the estate once its developed; but we foresee some buyers being hesitant to pay this amount, or are more inclined to wait for the 2020 launch of an EC at Tampines Ave 10.

Of course, compounding the issue is the tighter LTV (see point 1) and rising interest rates for bank loans (there are no HDB loans for ECs).

So, the lack of value ECs, combined with the lack of EC units in general, could leave some of our sandwiched Singaporeans or even those displaced persons from the 2017 en-bloc fever to choose bigger HDB resale units as an housing option.

[Recommended article: Executive condominiums: Are upcoming ECs in 2019/2020 worth the wait?]

- HDB could further reduce the number of BTO flats released in 2019

Earlier in 2018, HDB already announced that it was to launch 1,000 fewer BTO units than was originally planned for the rest of this year, citing stabilising HDB resale prices. If you dont see the euphemism here, well point it out to you: HDB is keen to moderate the supply of BTO flats to keep resale prices stable, moving forward.

Moreover, we are probably going to see a lot more launches for BTO projects in 2019 in non-mature estates (read: Tengah). Due to less than favourable locations plus lower odds of successfully balloting for a BTO flat with fewer units released, many BTO hopefuls are likely to give up and settle for a HDB resale flat, which isnt a bad thing given theyd have many more choices on where to live!

Would you like to stay in Tengah? (Were guessing no.)So, directly and indirectly, the government is giving the HDB resale market booster shots. This will continue in 2019, which could even have the effect of nudging the HDB resale price index up a little. After all, 2019 is looking very much like Election Year and, hey, what better way to give Singaporeans a reason to vote for

um

I mean, smile.

Whats your outlook for the HDB resale market in 2019? Voice your thoughts in our comments section or on our Facebook community page.

If you found this article helpful, 99.co recommends Why now is the best time to buy a HDB resale flat and 5 fatal mistakes Singaporeans make when upgrading to a condo

Looking for a property? Find the home of your dreams today on Singapores largest property portal 99.co!

Would you like to stay in Tengah? (Were guessing no.)So, directly and indirectly, the government is giving the HDB resale market booster shots. This will continue in 2019, which could even have the effect of nudging the HDB resale price index up a little. After all, 2019 is looking very much like Election Year and, hey, what better way to give Singaporeans a reason to vote for

um

I mean, smile.

Whats your outlook for the HDB resale market in 2019? Voice your thoughts in our comments section or on our Facebook community page.

If you found this article helpful, 99.co recommends Why now is the best time to buy a HDB resale flat and 5 fatal mistakes Singaporeans make when upgrading to a condo

Looking for a property? Find the home of your dreams today on Singapores largest property portal 99.co!

Reply With Quote

Reply With Quote