The following posts and replies by PMET are taken from http://forums.condosingapore.com/showthrea...2462#post132462

The first sentence is half correct but the last sentence isn't true. This is not how it works. UIRP (uncovered interest rate parity) applies to Singapore's Monetary Policy so the first sentence is half correct. However, Singapore's interest rate can increase without the US increasing theirs but this is complicated. Due to the principle of UIRP, there should be no arbitrage in the relationship between any two currencies. Thus, an increase or decrease in interest rate directly affects the exchange rate, and vice versa. For more info, read this post (especially the 2nd, 3rd & 4th paragraphs): http://forums.condosingapore.com/showpost....p;postcount=547Originally Posted by CCR

It is well known that MAS does not use interest rates as a monetary tool... They use age appreciation... Honestly if u ask me.... Interest rate here will not go up very high unless US unemployment rate goes down to at least 8% and even that, Singapore interest rates increase might not be that high as singapore is a financial centre and we are almost always flush with cash hence the banks a lot of money to lend so very competitive so must offer good rates or else money sitting in the bank vault earning nothing....

Yes, the weakening USD is why Singapore property prices continue to appreciate in spite of tough government measures. In addition, foreign funds find it profitable to invest in Singapore because the SGD is expected to appreciate against the USD. Also, their returns will be higher than the interest rates charged for borrowing the cheap USD (carry trade). This causes a chain reaction which leads to a stronger SGD and lower interest rate. Read more here: http://forums.condosingapore.com/showpost....p;postcount=197Originally Posted by amk

hah, my favorite topic

SOR is primarily a USDSGD forward implied rate. It's not really a "lending" rate. It's kind of like, you borrow USD, convert to SGD, then later convert back to USD to repay. It's almost like u r funded in USD. And it's very sensitive to fx. So when SGD appreciates, or is expected to appreciate, SOR drops. It's volatile like fx, but if you are brave, and firmly believe USDSGD will go down all the way, take SOR to capitalize on it. The thing is, USD can be affected not just by financials. Politics can make USD higher. For example the next time u see North Korea firing a missile, or Portugal in crisis, u will see USD shootup, which will make SOR shootup immediately. You have a very recent example. When Ben announced QE2, every one said USD will drop like hell. (Because any economics will tell you massive printing of money will devalue the currency) What happened instead is, because of the europe crisis, USD went up. At one stage USD was the best performer. Many houses lost money on this bet.

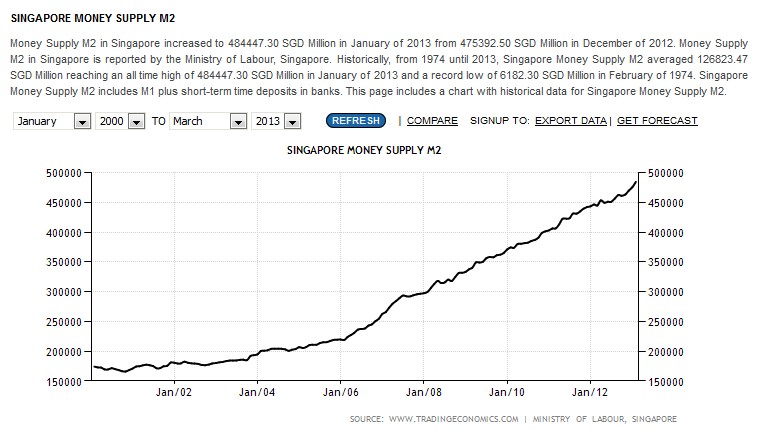

SIBOR is really a lending *benchmark* rate. That banks agreed to offer each other on this rate. It closely tracks the money supply of SGD and overall rate environment. It's "stable" because it has much less fx component. But since SGD is by and large a trading currency, it's still inherently tracking the USD rates. Without USD rates going high, no way SIBOR can be significantly higher.

Referring to the article titled Avoiding bubble trouble (http://forums.condosingapore.com/showthread.php?t=10681), the comment above is from one who doesn't understand the current situation (just like MAS).INFLATION is not flattering in a growing economy, and Singapore has been swinging against inflation by revaluation of the Sing dollar against major currencies especially the US dollar and the euro. It is taking a double-barrelled monetary tightening with an appreciation bias for the basket of currencies that the Sing sollar is pegged to.

Singapore'S economy grew by a whopping 14.7 per cent for the whole of 2010 and markets celebrated our city-state's leading role in Asia but such growth brought concerns such as long-term asset price inflation and depreciating worth of the Sing dollar. Arguably, a much stronger currency will save the worth of Sing dollar. The con, of course, will be the impact on competitiveness if the Sing dollar goes overboard to become too strong.

Though the government must allow for a very gradual and sustainable appreciation of the currency to help fight inflation, it must be mindful that working-class Singaporeans will be the worst hit in any inflationary impact. Their earning capacity will not grow proportionately to the inflationary growth, and their dollar will buy fewer goods and sundries. They have less flexibility and elasticity in fiscal prudence or imprudence and if the Budget 2011 does not provide for them specifically, the working class may be steps behind in Singapore's growth story.

Increasing tax reliefs to account for rising inflation and increased cost of living, exemption of essential items from GST, direct cash subsidies for conservancy charges or rental rebates, transport rebate for senior citizens and school-going children are probable remedies in Budget 2011 that could alleviate the temporal pains caused inadvertently by inflation. From the perspective of fiscal prudence, such measures will go a longer way towards helping the working class in Singapore. The blunt and brute force of any inflationary pressure can at least be lessened with a considerate Budget.

Lim Soon Hock

Managing Director

Plan-B ICAG Pte Ltd

Why letting the SGD appreciate isn't the solution?

When an economy grows normally without external influences (hot money), the demand is created internally thus inflation grows as people fight over a limited pool of resources. In this (normal) scenario, a stronger SGD makes everything cheaper (especially for imported products) and businesses slow because our products will be less competitive (economically).

However, in a case of hot money entering Singapore which directly creates demand and indirectly stirs up inflation (think: red-hot flushed stock market, property bubble, business investments, high COE prices and etc), an appreciating SGD creates more appetite for investments based in Singapore.

What happens when the hot money gets withdrawn in search of better returns elsewhere (when US/Europe recovers)?

Bubbles will burst! Stock market, property market, CAR COE, business investments, etc.

With regards to the above, there are two possible reasons why MAS is going with the "inflationary measure" (wrongfully allowing SGD to appreciate):

1. Political - China and most of ASEAN has been labeled by US as currency manipulating regimes. Singapore, with more than 14% growth last year, may be obliged to allow its currency to appreciate against the USD, lest that it gets condemned and "loose its global status".

2. Financial - The government may be enjoying the high taxes in the mist of all the inflation.

Just my 2cents

This post will be my last about the subject. Please help to spread the words around if you think that I'm right.

Reply With Quote

Reply With Quote